Trade Update | Will Mortgage Rates go lower by years end?

Fed Funds Rate forecast

Yesterday an individual called me after being referred to me by a mortgage lender about their question, ‘Will mortgage rates go lower by years end?’ . First, I was honored that this lender referred this individual to me about their question. And second, it brought to light how many people don’t understand and realize the scope of the Feds actions on the people of the United States and the world.

Let’s take a Second and Look back

During the Financial Crisis, Fed Chairman Ben Bernanke implemented, quantitative easing which injected money into economic system. When the effects of this action where not achieving his goals for the program in 2013, he proposed more QE. There where three sitting Board Governors that apposed the continuation of QE. One of them was the Chairman Jerome Powell. Chairman Powell’s position then was that continuous QE was not a smart idea.

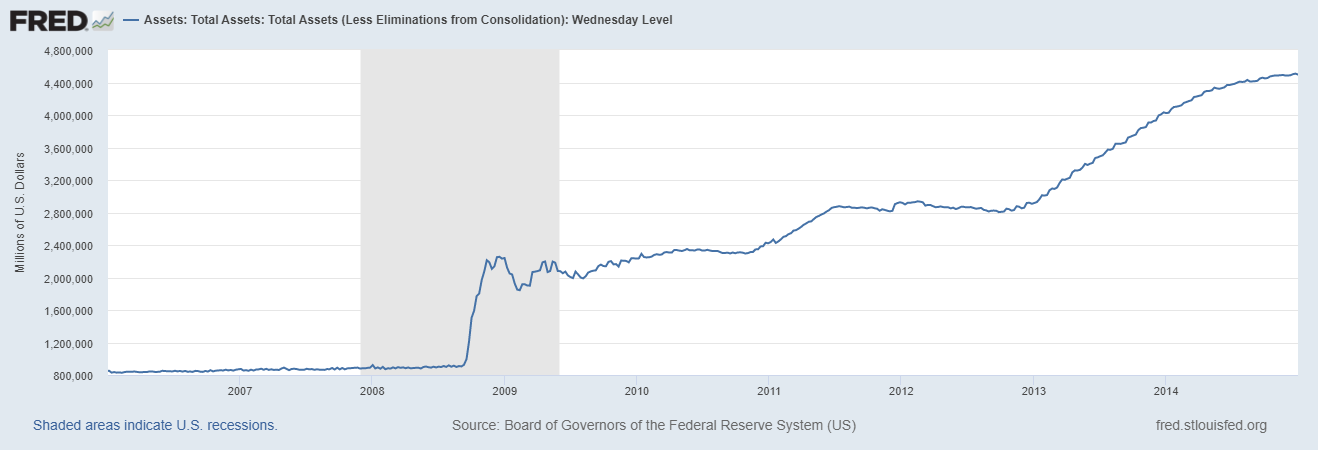

During Chairman Bernanke’s term 2006–2014, the Federal Reserves balance sheet expanded from $851 Billion to $4.4 Trillion.

According to the book “Lords of Easy Money”, this was a more than chairman had anticipated that the balance sheet would grow to. The Fed Funds rate during that same period went from a peak of 5.24% to a low of .12%. This amount of money being produced and the cost of that money effectively equaling zero % is why stock market growth grew.

This policy of easy money continued until January 2016 when Janet Yellen took over and began to raise rates until July of 2019.

The economy was not performing well so they believe a lowering of rates would create a more growth. The Feds Balance Sheet held steady and actually declined into December of 2019 one year after now sitting Chairman Powell enter as chairman.

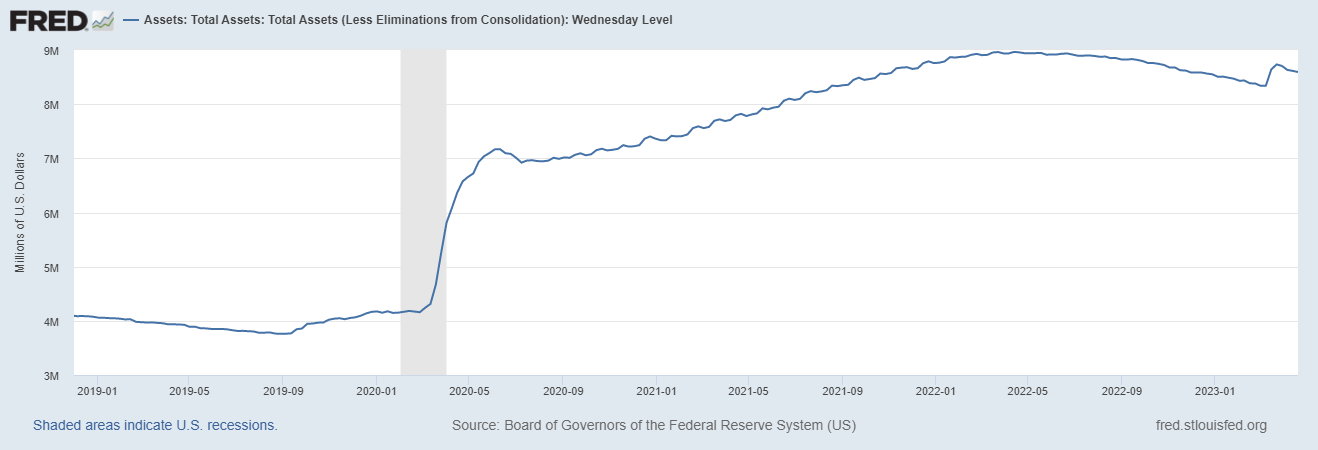

The the Pandemic change everything. To keep the economy afloat, a massive amount of QE was put into effect along with the lowering of Fed Funds rates back to .05%.

The Balance Sheet then went from a “Normal” $4 trillion to its peak in April of 2022 of $9 trillionish.

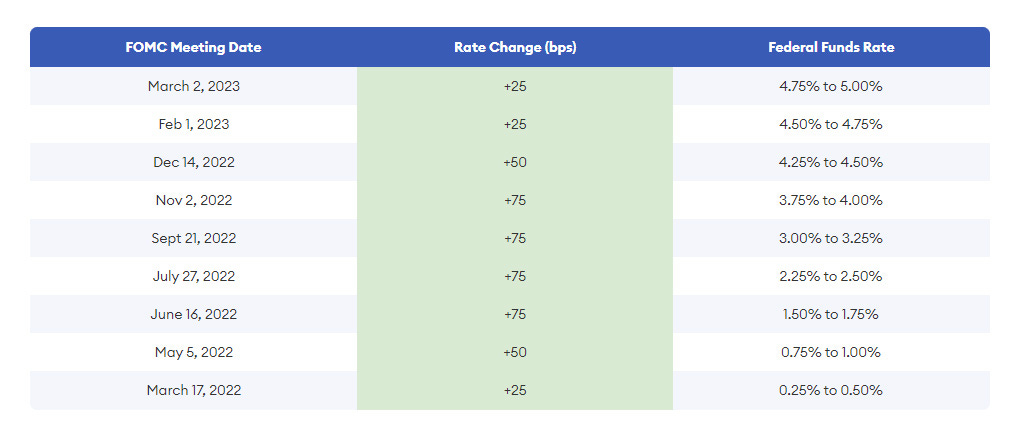

Since March of 2022 the Chairman Powell has raised rates at total of NINE times, taking the Fed Funds Rate to 4.65%. The last time the Fed was this aggressive was in 1928.

It takes between six to nine months after each raise for the economy to begin to feel the effects.

From my calculations we are just feeling the effects of the first 2 or 3 rate hikes. We have yet to feel the effects of the last 6 or 7. Next week it is anticipated that the Fed will raise another .25%. Inflation is still a problem in their eyes and unemployment is still low. So they will keep raising…until something breaks. And when it breaks…

So what did I tell the Individual who was referred to me?

Little background on this person. Great credit score, building a house, needs a construction loan and then convert it to a permeant loan.

I shared the above with this person. What I told them was the following.

Expect rates to go higher in the short-term

Expect the second quarter earnings of 2023 to be dismal in the financial sector and the high risk asset categories. This will put pressure of the Fed as we get further into the second half of 2023, but he won’t give right away.

Expect to see more bank closures into the 2nd half of 2023 and 2024. When that becomes a daily headline news story, the Fed language will change.

The Fed always over does it. Their economic models are lagging indicators and don’t front run the economic cycle.

Remember, 2024 is a Presidential Election year. If the Democrats what a second term, they can’t have a recession or a depression. Powell is a Republican. Think about that for a minute.

When the economic pot is boiling, the Fed will drop rates in a big way. 200 -300 bps. bring the Fed Funds rates down to 2% -3.5%. If they really over due it, we could see rates below 2%.

If mortgage rates get below 5% start pressuring your lender for a exceptional mortgage rate because of your stellar credit rating.

Be patient.

QQQTrade.CLUB Asset Allocation Update: Trades

Keep reading with a 7-day free trial

Subscribe to The Twelve to keep reading this post and get 7 days of free access to the full post archives.