Are Banks at Risk Again?

Did Silvergate Capital (SI) just start an Avalanche?

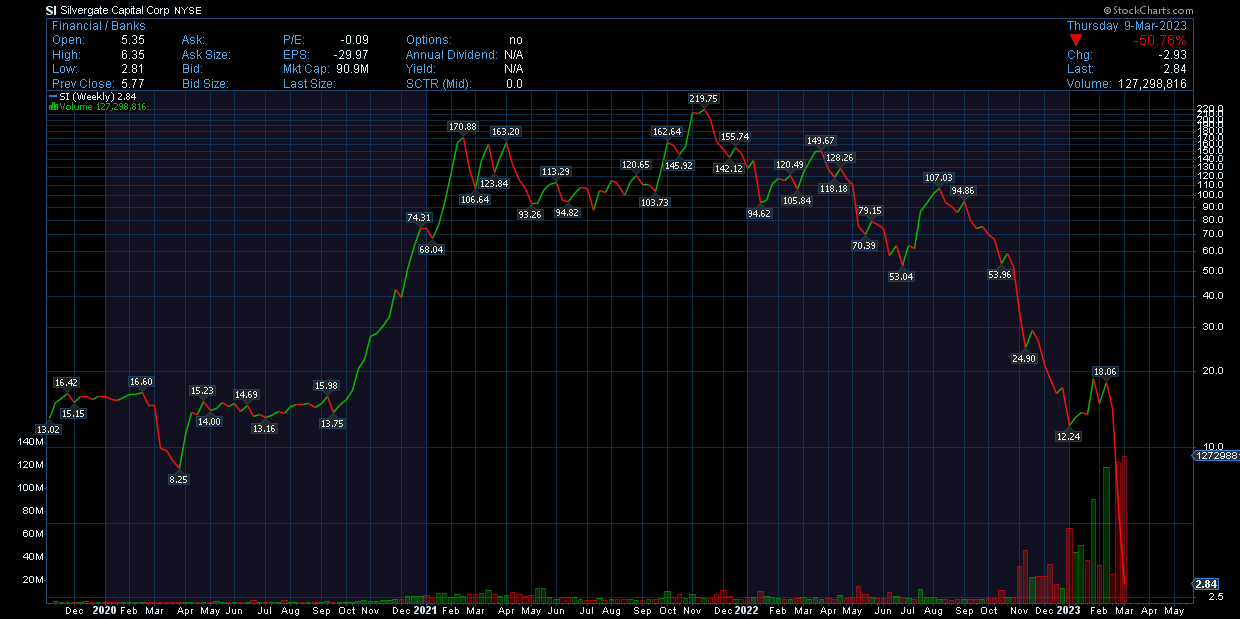

For those who don’t know who Silvergate (SI) is, they are a bank that made the headlines because of their focus on the crypto industry. They were made of up of 90% crypto deposits. Unless, you just got connected to the internet, crypto has been in the headlines for the last three years. Crypto is to the money systems as is the next coming of Christ is to Christians. Silvergate announced this week that it will voluntarily liquidate the banks assets and fold up shop.

The question that is being asked is, are they the only ones or is this going to spread like the Flu in a kinder garden class? Welllllllllll, Pat, I’ll take “Banks in a Pickle” for $500.

The same day that Silvergate announce that they were closing up shop, Silicon Valley Bank informed the world that its average deposit guidance would be down much less then their average and oh by the way, they are liquidating its entire $21 billion AFS portfolio. What is a AFS portfolio?

“Available for sale (AFS): A catch-all for debt and equity securities not captured by either of the above definitions. These are securities that the bank may retain for long periods but that may also be sold.” - Federal Reserve Bank of New York

Which now brings up another pretty chart that crossed my Twitter feed this morning at 5am.

This one comes from the FDIC. It shows the amount of Unrealize Gains and Losses that banks have on their investment securities portfolios. A bank has three types of investable assets.

Trading: Securities that are bought and held principally for the purpose of selling in the near term.

Held to maturity (HTM): Debt securities that the firm has the positive intent and ability to hold until maturity. (Equities can’t be included in this category since they don’t mature.)

Available for sale (AFS): A catch-all for debt and equity securities not captured by either of the above definitions. These are securities that the bank may retain for long periods but that may also be sold.

The problem that banks are facing now is not Credit Risk, but Interest Rate Risk. The Held to Maturity (HTM) category are Bonds. If a bank has bonds that they bought over the last 5 years, the bonds are now underwater and the losses are rising due to the rise in, you guessed it, the rise in Fed Funds rates.

2 yr Treasury

5yr Treasury

10yr Treasury

30yr Treasury

So what do they do? Hold them until maturity and get beaten up when they announce earnings because their investment portfolios are loosing money which means they are now bleeding money to pays competitive rates on their saving, money market accounts and CD’s? Or do they sell at a loss and roll that money into more competitive yielding assets?

It is estimated that the banks are looking at >$1 TRILLION loss on their securities portfolio. Time to buy banks? AAA…no. BUT! will there be an opportunity to buy those that take the hit from wall street and get there house in order in the future?

History note. Today is the anniversary of the Dot.com Bubble peaking in March 2000.

Subscribers, I am close to having your Intermediate Term Asset allocation model ideas ready for print. Sorry for the wait.

Have good weekend.