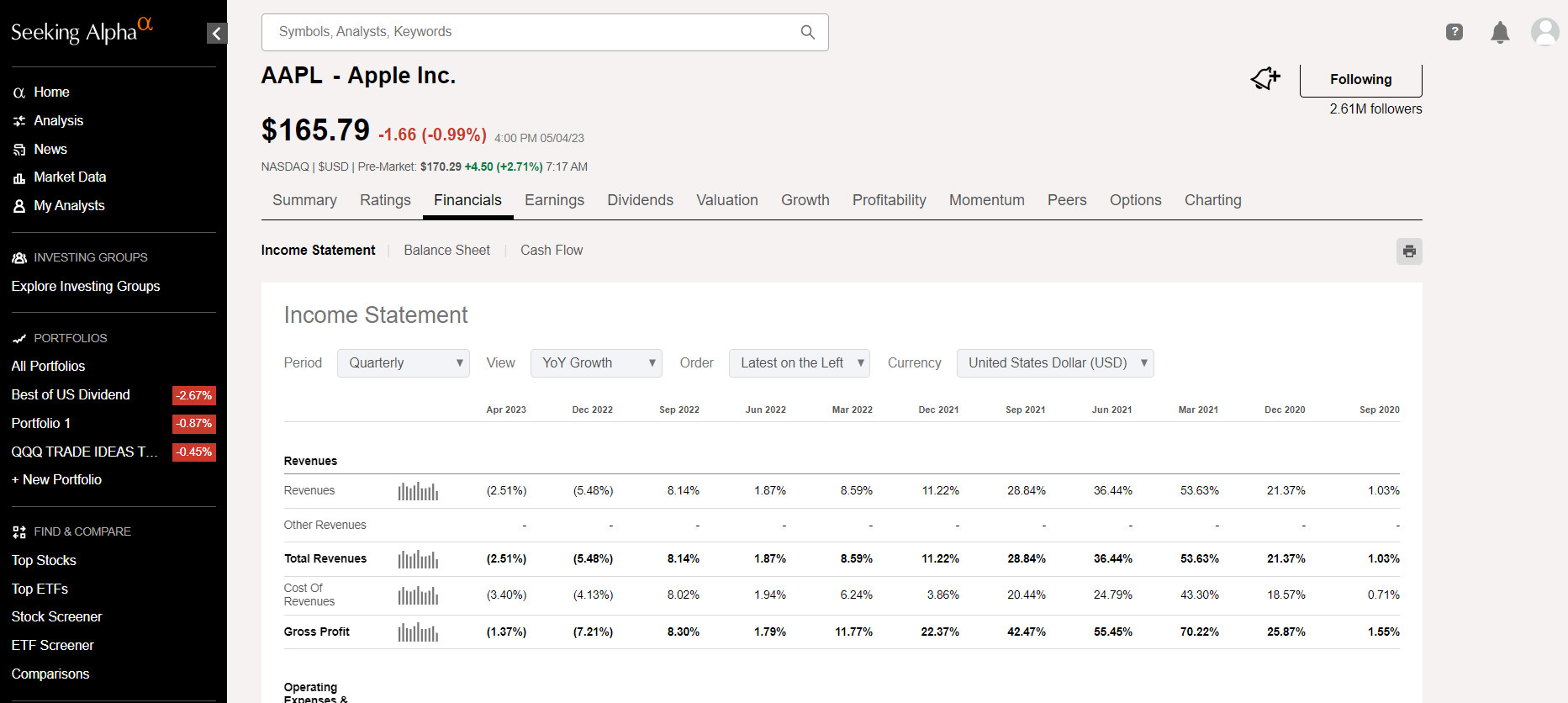

Apple Beats, Yield Curve Rises

Is Apple going to save the day?

Apple reported earning after the bell beating estimates:

EPS: $1.52 per share vs. $1.43 expected

Revenue: $94.84 billion vs. $92.96 billion expected

Gross margin: 44.3% vs. 44.1% expected

According to CNBC, these are the individual product line breakdowns:

iPhone revenue: $51.33 billion vs. $48.84 billion expected

Mac revenue: $7.17 billion vs. $7.80 billion expected

iPad revenue: $6.67 billion vs. $6.69 billion expected

Other Products revenue: $8.76 billion vs. $8.43 billion expected

Services revenue: $20.91 billion vs. $20.97 billion expected

When I look at it from a YoY perspective, i’m seeing something a bit different:

Revenue on a Quarterly YoY is down (2.51%). Gross profits down (1.27%).

Net Income Quarterly YoY down (3.40%).

Maybe I’m not looking at this the right way? I look at the year over year vs what they share on the big news channels. From my perspective, Apple is like every other company, revenue and earnings are slowing.

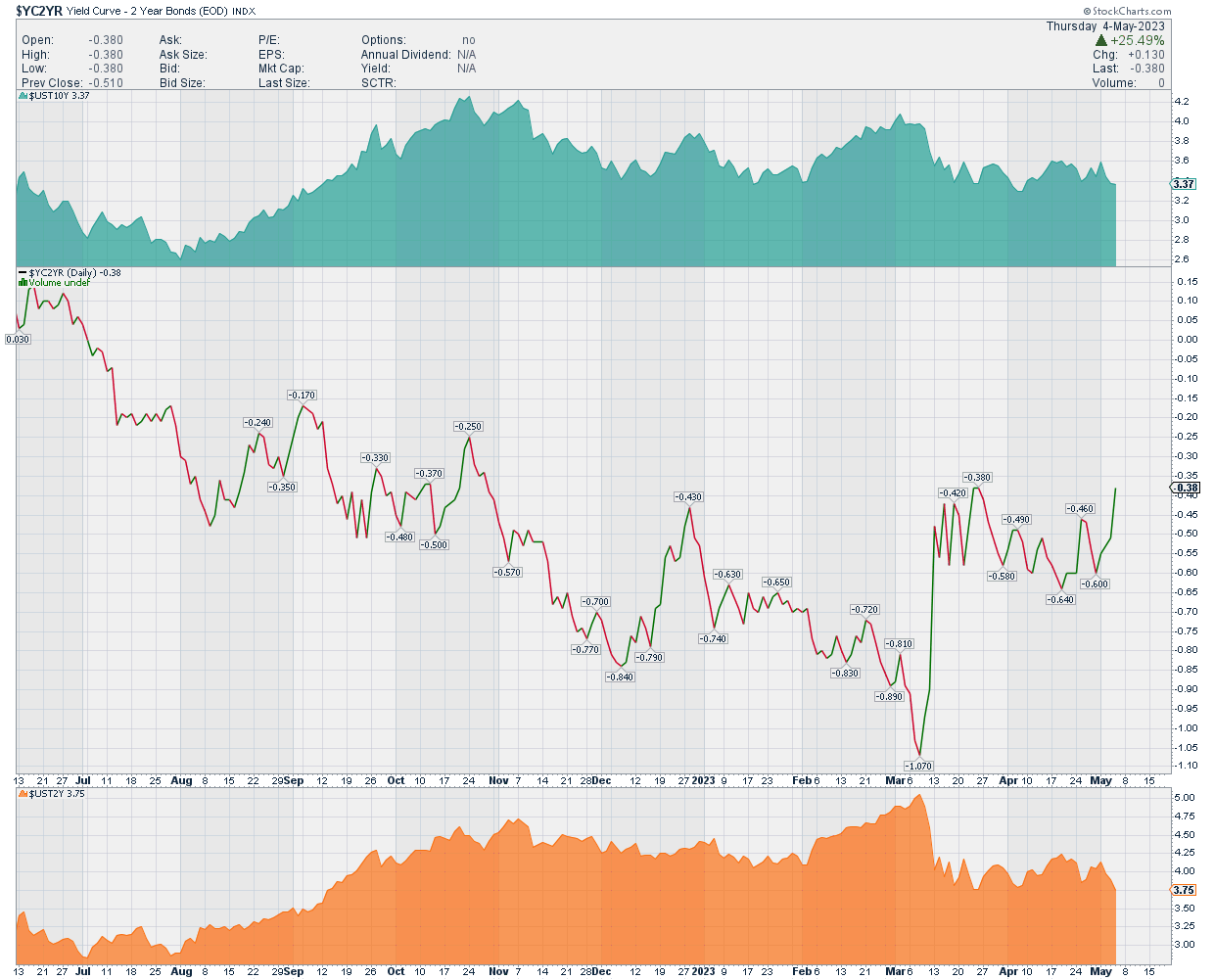

Yield Curve

Treasury’s have seen a sizeable amount of inflows YTD. iShares 20+year Treasury Bond ETF (TLT) has seen inflows of $7.18 billion. TLT closed 2022 out at $98.56 and closed yesterday at $105.24.

Yield Curve has moved up due to the rush into long duration bonds. Close yesterday at -0.38%. Better then when Silcon Valley Bank collapse at -1.07%. But we may see another bank bite the dust this weekend.

PacWest Bancorp is looking for a buyer.

Conclusion

Even though it looks like Apple saved the day, banks on a market to market basis are insolvent as a hole. That’s not a problem that Chairman Powell solves over night by lowering interest rates. The Fed has done the damage and I wonder if that is intention.

Paid Subscribers

Keep reading with a 7-day free trial

Subscribe to The Twelve to keep reading this post and get 7 days of free access to the full post archives.